Egypt-Arab Gulf Countries: Strategic Synergies, Not Political Alignment

The relationship between Egypt and the Arab monarchies in the Persian Gulf – particularly Saudi Arabia, United Arab Emirates, and Qatar – has acquired renewed strategic significance in the context of the ongoing crisis involving the United States, Israel, and Iran. What emerges is a pattern of structural yet asymmetric interdependence, in which Cairo remains highly vulnerable to external shocks while retaining sufficient political adaptability and diplomatic relevance to avoid marginalisation.

The war affects Egypt primarily through indirect transmission mechanisms, rather than direct exposure. This is the key causal hinge. Egypt’s economic model depends fundamentally on the Gulf’s ability to generate liquidity, stability, and political backing. When that capacity is strained – due to heightened security risks, financial volatility, and the need for internal resource mobilisation – the repercussions for Cairo become immediate and systemic.

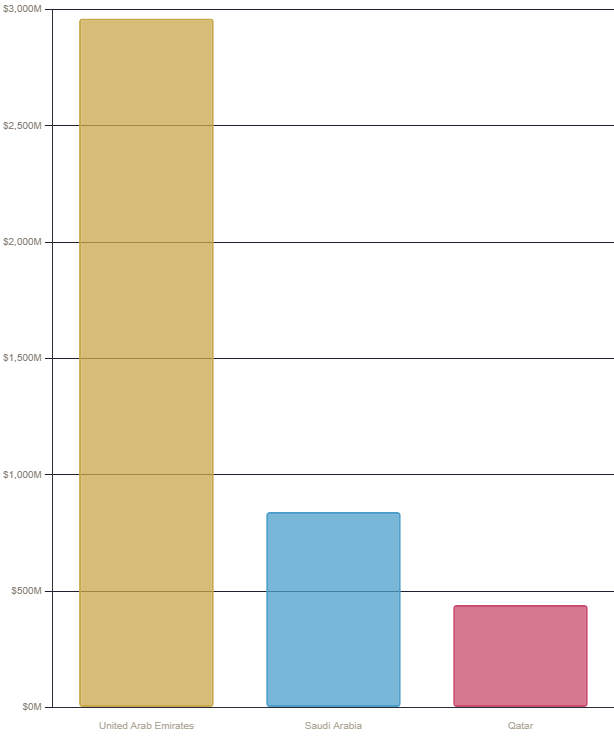

This dependence has deepened significantly over the past decade and is empirically measurable. Since 2013, Gulf countries have provided Egypt with well over $100 billion in financial support, including central bank deposits, grants, and investments. More recently, the United Arab Emirates committed $35 billion to the Ras el-Hekma project in 2024, while Qatar has moved toward a $7.5 billion investment package in 2025. At the same time, Gulf sovereign wealth funds have expanded their presence in Egypt through acquisitions in banking, infrastructure, and state-owned enterprises, signalling a transition from emergency support to structural economic entrenchment.

Yet this growing dependence has not translated into rigid political alignment. On the contrary, the relationship remains fundamentally instrumental and adaptive: Egypt cooperates closely with Gulf partners while deliberately preserving strategic flexibility, aware that excessive alignment would heighten its exposure to regional shocks.

Vectors of Exposure: Egypt’s Structural Dependencies

The most immediate transmission channel is financial. As Saudi Arabia, United Arab Emirates, and Qatar reallocate resources to safeguard domestic stability, their capacity to support Egypt becomes more constrained and conditional. This shift is particularly consequential given Egypt’s macroeconomic fragility: external debt has exceeded $160 billion, and financing needs remain structurally high. Gulf monarchies’ support does not disappear, but it becomes more selective, more politically contingent, and increasingly tied to strategic returns. In this sense, the war risks transforming the Gulf from a systemic stabiliser into a conditional backstop.

A second transmission channel is commercial. Egypt is deeply integrated into Gulf markets, which account for over one-third of its exports to the Arab world, with Saudi Arabia and the United Arab Emirates among its largest regional partners. Conflict-induced increases in transport and insurance costs, combined with disrupted logistics and weaker demand, can sharply reduce export flows. This constrains access to hard currency precisely when Egypt’s external position is under strain.

The energy channel further amplifies this asymmetry. Escalation involving the United States, Israel, and Iran fuels global energy volatility and price increases. For Egypt – still a net importer in key segments – this translates into rising fiscal pressure and inflation. The country’s monthly gas import bill has surged from roughly $500-600 million to as much as $1.5-1.6 billion during periods of heightened instability. While some Gulf economies can offset risks through increased hydrocarbon revenues, Egypt experiences the opposite dynamic, with direct implications for domestic stability.

Remittances constitute another critical link. Egypt is one of the world’s largest recipients, with inflows reaching a record $41.5 billion in 2025, a significant portion originating from workers in Gulf economies. Any slowdown in GCC economic activity – due to conflict-related uncertainty – feeds directly into lower remittances, weaker domestic demand, and reduced foreign currency inflows. This reinforces the indirect but deeply embedded nature of Egypt’s vulnerability.

The logistical-maritime dimension adds further pressure. The Suez Canal – historically generating over $9 billion annually – is exposed simultaneously to instability in the Persian Gulf, disruptions around the Strait of Hormuz, and tensions in the Red Sea. Recent shocks have already shown how revenues can decline dramatically under stress. In a context of regional escalation, rising insurance premiums and rerouting of global shipping flows risk undermining one of Egypt’s key external buffers.

An Indispensable Actor. Egypt Cautiously Recalibrating its Regional Posture

Within this constrained economic framework, the political-diplomatic dimension becomes even more consequential. Despite its vulnerabilities, Egypt retains a distinctive regional asset: a long-standing role as a mediator, rooted in decades of engagement with the Israeli-Palestinian conflict. Cairo has built significant diplomatic capital as a credible interlocutor among otherwise irreconcilable actors, including Israel, Palestinian factions, and international stakeholders. This role, shaped since the Camp David Accords and reinforced over time, grants Egypt a level of negotiating legitimacy that exceeds its economic weight.

This diplomatic relevance extends beyond the Palestinian file. In the context of the recent Islamabad talks between the United States and Iran, Egypt played a supporting but meaningful role within a broader mediation ecosystem, contributing to backchannel coordination and efforts to sustain dialogue. This reflects a recurring pattern: Cairo may not always lead negotiations, but it consistently operates as a secondary yet indispensable diplomatic node.

At the same time, Egypt’s diplomatic weight is closely linked to its strategic value for the Gulf. Beyond political mediation, Cairo has historically functioned as a security partner and stabilising force within the Arab system. Its military capacity, geographic position between the Mediterranean and the Red Sea, and control of critical chokepoints make it a key element in Gulf security calculations.

However, the current crisis highlights a notable shift. Despite its structural importance, Egypt has adopted a cautious and restrained posture. This should not be interpreted as diminished relevance, but rather as evidence of a deliberate and prudent process of strategic recalibration. Cairo appears intent on limiting its exposure, particularly given the risk that escalation could reignite maritime insecurity in the Red Sea – an outcome that would directly threaten both trade flows and domestic stability.

This behaviour reflects a dual logic. On the one hand, Egypt remains a pillar of regional security, whose stability underpins broader Gulf resilience. On the other, it is increasingly wary of overextension, given that the costs of instability are disproportionately internalised. The recent disruptions to Red Sea shipping and their impact on Suez Canal revenues have reinforced this cautious approach.

This calibrated restraint strengthens Egypt’s broader diplomatic posture. By avoiding rigid alignment or overt militarisation, Cairo preserves its credibility as a mediator and maintains flexibility across multiple diplomatic tracks. It continues to engage with Gulf partners, coordinate with Washington, and remain relevant in dialogue channels involving Iran-linked actors – without becoming directly entangled in escalation dynamics.

Ultimately, the current crisis highlights the central paradox of Egypt’s regional position. The country is simultaneously a security asset for the Gulf countries and a dependent actor within its economic orbit; a recognised mediator and a state constrained by structural vulnerabilities. In this context, Egypt pursues a strategy of selective engagement: remaining present and influential, while deliberately avoiding front-line exposure.

Egypt thus emerges as a paradoxical but indispensable actor – indirectly affected by the war through Gulf exposure, yet still capable of shaping regional outcomes through diplomatic leverage and adaptive non-alignment.

Giuseppe Dentice